The table of content

This article is a summary of the scientific work published by Anatolii Kolot, Oksana Herasymenko, Anna Shevchenko, Ivan Ryabokon

The original source can be accessed via DOI 10.33111/nfmte.2022.072

Introduction

Technological acceleration, data ubiquity, demographic realignments and always-on connectivity are quietly rewriting the fundamentals of economic growth and management. These forces ripple through every layer of production, reshaping the social division of labour, altering organisational structures and redefining what economically active people value. In their wake emerges a network society and a radically different world of work.

At the centre of this shift lies employment in its broadest sense—every socially organised form of labour that links individuals to economic output and civic participation. Yet the human consequences of this transformation remain only partially mapped. Many forecasts still frame automation as a countdown to widespread job loss, while others proclaim a friction-free rise of “post-scarcity” work. Both extremes overlook the complex interplay of structural and behavioural variables now reshaping labour markets.

Conventional scholarship has already moved beyond first-generation descriptions of market volatility, regulatory levers and skill polarisation, but it continues to analyse each theme in isolation. New realities demand a holistic, predictive framework—one capable of capturing both the fresh competitive advantages and the latent vulnerabilities of the workforce in the digital age. The research underpinning this article answers that call by combining interdisciplinary methods with economic-mathematical modelling to reveal patterns that remain hidden in more fragmented analyses.

Several intertwined dynamics temper the raw displacement effect of automation and, in many contexts, reverse it. Demographic turnover and local labour-market imbalances are reshaping talent pools faster than intelligent machines can replicate them. Meanwhile, non-standard work formats—remote, freelance and project-based arrangements—are expanding participation beyond the confines of traditional contracts. Flexible working-time models are dissolving the historic dichotomy between work and leisure, prompting firms to recast productivity metrics around outcomes rather than hours.

Entirely new industries are also poised to deliver goods and services that today’s forecasting tools struggle even to name, while cost-benefit realities and ethical safeguards ensure that several sectors will remain only partially automated for years to come. Underpinning all of these shifts is an evolving hierarchy of social values in post-industrial societies, a realignment that increasingly shapes where, how and—crucially—why individuals choose to engage in paid work.

By integrating these dynamics, the study proposes an employment model grounded in human-centred development. Digitalisation, in this view, is less a march toward a jobless future than an invitation to redesign institutions, training systems and policy incentives so that employment retains its status as a core social value. Adaptability—at the level of firms, workers and entire economies—emerges as the defining competitive edge, enabling societies to convert technological change into sustainable, broadly shared prosperity.

The sections that follow detail the model’s assumptions, supporting evidence and strategic implications. In place of dystopian alarms or utopian promises, the discussion offers a practical blueprint for navigating labour-market turbulence while keeping humans, not algorithms, at the heart of economic progress.

Why Digital Transformation Rewrites the Rules of Work

Over the past two decades, digital technologies have spread from isolated use-cases to every layer of production and service delivery. Cloud platforms, advanced analytics, robotics and artificial intelligence now execute tasks—in real time and at scale—that once demanded physical presence or manual oversight. As the Fourth Industrial Revolution gains pace, its most disruptive effects are surfacing not in product design or marketing strategy, but in the mechanisms that match people to work.

Data published by the European Jobs Monitor already points to a decline in roles built around routine, codified activities. Automation can absorb many of these functions at lower cost and higher speed, yet the same data also show pockets of resilience. Occupations that hinge on situational dexterity—caregiving, certain trades, food preparation—are considerably harder to digitise, even when skill requirements appear modest. At the opposite end of the spectrum, demand is rising for specialised talent that can architect, secure and fine-tune digital systems. Wage pressure is following the same trajectory, rewarding advanced proficiency and punishing static skill sets.

Continuous learning has shifted from optional to existential. The competencies prized by recruiters today may expire within a planning cycle, leaving experienced staff under-prepared for adjacent roles created by the very technologies that displace them. Economic modelling by McKinsey suggests that in roughly 60 percent of occupations, one-third of current tasks could be delegated to software or machines. Career durability therefore depends less on deep expertise in a single procedure than on the capacity to acquire and recombine new digital skills at speed.

Comparative studies across China, the United States and the European Union confirm that automation risk varies sharply by sector, by country and even by region. Job clusters dominated by repetitive motion or codifiable decision-trees—assembly, basic logistics, routine back-office processing—face the highest displacement probabilities. Conversely, roles anchored in abstract problem-solving, interpersonal persuasion or creative synthesis tend to convert technology into a force multiplier rather than a substitute. These asymmetries explain why forecasts about the “end of work” diverge so widely: each projection depends on which segments of the labour market are placed under the microscope.

Two opposing narratives currently shape public policy and boardroom strategy. One projects mass technological unemployment and promotes unconditional basic income as a social stabiliser. The other anticipates that AI-augmented workflows will expand global employment by unlocking latent demand and spawning new categories of economic activity. Evidence to date supports neither extreme in full. Automation is eliminating jobs at the task level while creating fresh demand for complementary roles in data stewardship, human-machine interface design and cross-platform orchestration. Long-term outcomes hinge on education systems, labour-market flexibility and migration policy—factors that sit largely outside the technology domain.

A separate but related trend is the formalisation of “digital employment” as a recognisable labour model. Four attributes define this modality:

- Digital infrastructure—cloud, APIs and collaboration software—constitutes the core production environment.

- The output is itself a digital product or service, from software code to automated translations.

- Work processes rely on continuous data exchange rather than sequential hand-offs.

- Compensation, reporting and compliance run on digital ledgers and online platforms.

Within this umbrella, researchers differentiate between basic digital employment (performing prescribed tasks with standardised tools) and smart digital employment, where teams engineer or refine digital products to meet novel, measurable objectives. Smart roles demand a higher degree of abstract thinking and carry greater economic upside—but they also assume advanced training and an appetite for self-directed learning.

Remote and project-based contracts give digital workers unprecedented control over time and location, yet these benefits arrive bundled with structural vulnerabilities: inconsistent income streams, limited legal safeguards and blurred work–life boundaries. Professional mastery offers some buffer against these risks, but it rarely substitutes for pensions, healthcare or collective bargaining. Companies that depend on fluid talent pools therefore face mounting pressure to develop hybrid welfare models—either in partnership with governments or through private benefit schemes that attract scarce specialists without binding them to legacy hierarchies.

Digitally mediated employment is gaining critical mass in high-tech verticals—software, financial services, advanced manufacturing—and its spill-over effects are material. Regions that host dense networks of digital professionals report faster productivity growth and a stronger startup pipeline, raising the baseline for national competitiveness. Conversely, jurisdictions slow to upgrade digital infrastructure or lifelong-learning programs risk entrenching structural unemployment, even if headline automation rates appear modest.

Research Methodology

The empirical framework for this study rests on systemic and interdisciplinary methods that fuse insights from labour economics, innovation theory and data science. This composite lens allows the analysis to capture both the enabling and the destabilising forces that digitalisation introduces into employment markets. The guiding premise is that shifts in labour practices, job volume and occupational mix unfold along two transformational vectors—constructive and destructive—and that the balance between them varies by industry, skill intensity and national context.

Central to the investigation is an occupational taxonomy that sorts jobs into four broad groups according to their exposure to digital technologies. At one end of the spectrum sit the “rising stars,” occupations whose demand trajectory climbs in tandem with advanced analytics, cloud infrastructure and automation. At the opposite extreme are the “dying professions,” roles whose core functions are increasingly absorbed by software and smart machines, thereby compressing headcount requirements. Between these poles lie two intermediary groups that experience partial augmentation rather than outright displacement. The taxonomy serves as a practical instrument for tracing how constructive and destructive pressures manifest across distinct labour segments.

To test the hypothesis that digitalisation reshapes employment in both scale and structure, the study employs cluster-analysis techniques drawn from multivariate statistics. Socio-economic and socio-labour indicators—ranging from digital-skill penetration and capital intensity to wage dispersion and job-creation velocity—feed into an algorithmic process that groups industries sharing similar transformation patterns. By revealing hidden affinities, the clustering exercise identifies which sectors gravitate toward high-tech, innovation-led growth and which drift toward contraction under equivalent technological conditions.

The methodology recognises that technology is not the sole driver of labour-market outcomes. Regulatory frameworks, education systems, demographic profiles and cultural attitudes toward work all act as moderators that can amplify or dampen digitalisation’s impact. Accordingly, the analytical model incorporates control variables for these contextual factors to isolate the net effect of technology on employment trajectories. The resulting evidence base supports a more nuanced reading of the future of work—one that moves beyond deterministic predictions and instead maps a spectrum of possibilities shaped by strategic, policy and human-capital choices.

Results

In assessing how technology and demographics will reshape labour markets over the next two decades, recent projections by the International Labour Organization and allied studies indicate that automation alone could place almost half of current U.S. jobs at risk of displacement, threaten a majority of positions across the ASEAN-5 bloc, and expose up to two-thirds of roles in developing economies to varying degrees of task substitution. Even in advanced OECD countries, where only about one job in ten faces a high probability of full automation, between one-half and two-thirds of existing occupations are expected to undergo substantial re-engineering as software and smart machines absorb routine components of daily work. Corporate surveys echo these findings: roughly one company in two anticipated shrinking full-time head-count by 2022 as digital systems scaled. Parallel demographic trends add a second layer of complexity. Dependency ratios—the number of young and elderly residents relative to the working-age population—are forecast to climb steeply across Europe, North America, Asia, Oceania and Latin America, signalling tighter labour supplies and higher social-security burdens, while Africa is projected to experience the opposite dynamic of a rapidly growing, youthful workforce. Together, these forces suggest a future employment landscape defined not merely by job destruction or creation in isolation, but by a fundamental redrawing of occupational structures, skill requirements and regional talent flows.

The data consolidated in Table 1 offer a concise snapshot of these intersecting pressures, clarifying both the scale of potential task automation and the divergent demographic trajectories that will shape how different regions experience—and respond to—digital transformation.

Demographic dynamics are increasingly recognised as a structural force behind the re-configuration of labour markets. Slower population growth, longer life expectancy, falling birth rates and the corresponding rise in dependency ratios have already begun to erode the relative size of working-age cohorts in many economies. At the same time, intensified migration flows and the large-scale entry of women into paid employment are offsetting part of that contraction, creating highly asymmetrical labour-supply patterns from one region to the next. These cross-currents yield a paradox: aggregate population trends may appear benign, yet employers in numerous sectors report mounting shortages of young and mid-career talent. International Labour Organization data highlight the effect. After a sharp pandemic-related dip in 2020, labour-force-participation rates have rebounded globally and within the EU-27, whereas Eastern Europe continues to face a steady decline; Ukraine, which experienced a deeper fall, shows early signs of recovery but remains below its pre-crisis trajectory. The divergent paths underscore how demographic headwinds combine with region-specific shocks to reshape both the quantity and the quality of available human capital.

Recent employment metrics provide additional nuance to the demographic findings. International Labour Organization datasets—covering actual results from 2001 to 2021 and model-based projections through 2023—show that the share of working-age adults holding jobs has remained broadly resilient, even in regions grappling with shrinking labour pools or elevated geopolitical risk. Global employment hovered near 60 percent at the turn of the century and, despite cyclical dips, is expected to stabilise rather than contract over the next two years. A similar pattern emerges across Europe: Northern, Southern and Western member states have pushed their employment-to-population ratio above pre-pandemic levels, while Eastern Europe’s long-term recovery moderated but did not reverse. Ukraine’s trajectory diverged sharply during 2020 yet displays a modest rebound in the latest forecasts.

Unemployment trends reinforce this cautiously optimistic outlook. Global joblessness has trended downward since 2009, and regional aggregates for both the EU-27 and Eastern Europe point to further easing through 2023. Northern, Southern and Western Europe, once scarred by double-digit unemployment, now project single-digit rates in the medium term. Even Ukraine—whose labour market absorbed multiple external shocks—shows an anticipated decrease in unemployment relative to the 2020 peak. These data collectively challenge “jobless future” narratives by illustrating that, although task profiles are shifting and certain occupations are disappearing, aggregate demand for labour has proved unexpectedly sticky.

Taken together with participation-rate dynamics (see Figure 1), the evidence suggests that advanced automation and demographic headwinds are not translating into wholesale employment collapse. Instead, they are recasting the composition of work, tilting rewards toward adaptable skills and digitally enabled roles. Policymakers and business leaders therefore face a dual imperative: accelerate retraining to match emerging job architectures while reinforcing labour-market institutions that can weather future shocks without triggering systemic unemployment.

Digitalisation operates less as a linear disruptor and more as an all-encompassing field of forces that compress, stretch and reconfigure the fabric of work in real time. At the heart of these dynamics stands a “competence market” in which knowledge, skills and technological capacity are continuously repriced against one another. Within this arena, two transformational vectors determine employment outcomes. Filling effects channel the constructive side of change: advances in AI, sensor networks and cloud computing expand the frontier of economically viable tasks, usher in sectors such as immersive design, quantum-secure logistics and bio-informatics consulting, and raise output per hour in occupations once constrained by analogue bottlenecks. These gains translate directly into new hiring pipelines, entrepreneurial niches and a more diversified spectrum of career paths—collectively designated an employed future. Substitution effects, in contrast, give destructive change its bite. As algorithmic decision systems mature, they appropriate routine cognitive and manual functions, hollowing out job families centred on predictable workflows and depressing demand for legacy competences that machines can replicate more cheaply and at scale. The resulting displacement fuels the spectre of an unemployed future populated by “dying professions.”

Figure 4 situates these countervailing forces inside a single system diagram. Digital-economy drivers flow inward, triggering a set of transformational effects that fan out along constructive and destructive channels. On the left, the filling pathway illustrates how the emergence of hybrid professions—cyber-forensic auditors, generative-AI ethicists, drone-fleet coordinators—absorbs labour released from traditional roles while simultaneously boosting productivity in those that remain. On the right, the substitution pathway tracks the mechanical reassignment of tasks once handled by humans—claims processing, basic language translation, parts of legal discovery—to autonomous platforms. The diagram further highlights a critical feedback loop: whether a labour market tilts toward employment creation or erosion depends not solely on technology but on the speed at which education providers, employers and policy makers recalibrate incentive structures, credential frameworks and social-protection instruments.

This systems view challenges analyses that isolate job loss from job creation or that treat digitalisation’s upside as a temporary anomaly before an inevitable wave of automation. Instead, it points to a dynamic equilibrium in which constructive effects can match or outweigh destructive ones—provided that institutional agility keeps pace with technological acceleration. Forward-looking strategies therefore pivot on three levers: rapid reskilling aligned with emergent competence clusters, adaptive labour regulations that recognise portfolio and remote work as mainstream formats rather than exceptions, and innovation policies that funnel research funding toward human-complementary technologies rather than purely labour-saving devices. By framing digitalisation as a contest of simultaneous “filling” and “substitution” pressures, the Employment-XXI model opens the analytical space needed to design interventions that tilt the balance toward inclusive, productivity-led growth instead of zero-sum displacement.

Across 2013-2020 the high-tech and export-oriented industries tracked in the database follow a clear three-way pattern that supports the article’s broader thesis about “rising-star” and “dying” job clusters.

1. Employment scale versus wage premium

Large, traditional export pillars—food processing and metallurgy—continue to employ the greatest head-counts (well above 250 000 full-time staff each in the early years), yet their average monthly wages hover just above the national mean. By contrast, digital-intensive activities such as computer manufacturing, telecommunications and R&D sustain far smaller workforces (typically 20 000-120 000) but pay 1.5-2.0 × the country-wide salary benchmark, and that premium widens over time.

2. Output and value-added momentum

Inflation-adjusted output and gross value added expand fastest in the computer, telecom and pharmaceutical segments, outpacing the broader economy even during the contraction in 2014-2015. Chemicals and metallurgy record flatter trajectories—and in several years outright declines—underscoring their vulnerability to technology-driven substitution and commodity-price swings.

3. Profitability dispersion

Pharmaceuticals consistently post the highest gross-profit figures and healthy margins, reflecting pricing power in specialised global markets. Telecom maintains solid but more volatile profit growth, while chemicals oscillate between modest gains and occasional losses. Food and metallurgy show the thinnest margins, signalling limited room for wage growth without productivity breakthroughs.

4. Workforce formalisation trends

The share of non-registered or contract-based labour falls steadily in high-tech services (telecom, R&D) and computers, hinting at professionalisation and tighter compliance. Export-heavy food and metals keep the highest proportions of non-registered workers, pointing to ongoing informality pressures in low-margin, labour-intensive operations.

5. Productivity inflection

When output and value added are normalised by employee count, computers, telecom and pharmaceuticals deliver the steepest productivity gains, confirming digitalisation’s constructive “filling effect” in those niches. Metals and chemicals lag behind, exemplifying the destructive “substitution effect” where capital-deep technologies replace labour without a corresponding surge in high-value output.

6. Resilience through external shocks

During the 2014-2016 geopolitical and currency shocks, employment in computers, telecom and pharmaceuticals remains comparatively stable, whereas food and metallurgy shed staff rapidly. The ability of high-tech segments to preserve head-count while lifting real wages underscores their strategic role in cushioning macroeconomic volatility.

Taken together, the dataset illustrates how digitalisation amplifies divergence: high-tech, knowledge-intensive industries generate fewer but better-paid jobs and stronger productivity growth, while large, resource-dependent sectors struggle to defend margins and formal employment. These patterns validate the hypothesis that occupational demand is bifurcating—with “rising-star” professions gravitating toward digital clusters and “declining” roles concentrated in traditional, labour-heavy value chains.

The self-organising map in Figure 5 visualises how eight strategically important industries in Ukraine’s economy group according to a composite profile of workforce size, employment structure, wage dynamics and value-generation capacity over the 2013-2020 horizon. Seven discrete clusters emerge. At the technological frontier sits Research & Development, occupying its own node and underscoring the sector’s singular combination of small head-count, top-tier salaries and high value added per employee. Pharmaceutical manufacturing forms a second, equally cohesive cluster, confirming that scale efficiencies and intellectual-property intensity set it apart from the rest of manufacturing. Telecommunications bifurcates across two adjacent clusters: observations up to 2017 appear alongside other information-service activities, while the 2018-2020 data migrate into a corner cluster, signalling a late-decade surge in both wages and productivity that distances the sector even from its historical baseline.

At the opposite extreme, food processing occupies an isolated cluster with the largest workforces but the lowest wage-to-output ratios, highlighting a labour-intensive model vulnerable to automation-driven substitution. Metallurgy constitutes its own mid-sized cluster, reflecting moderate employment contraction and profitability pressure yet retaining higher capital intensity than food production. The most heterogeneous cluster groups computer and optical-equipment manufacturing, electrical-equipment manufacturing and chemical production. These activities share medium-scale employment, rising—but not yet premium—salary levels and a transitional position between traditional export platforms and fully digital value chains.

The spatial arrangement on the map therefore mirrors the article’s broader thesis: digitalisation intensifies divergence. Innovation-centric sectors (R&D, telecom post-2018, pharmaceuticals) gravitate toward clusters characterised by compact workforces, high real wages and robust value creation—archetypal “rising-star” environments. Legacy export pillars (food, metallurgy) consolidate in clusters defined by large head-counts and thin margins, aligning with the “dying-profession” risk profile. Transitional industries in computing, electrics and chemicals occupy a liminal cluster where targeted upgrades in digital capability could tip the balance toward constructive outcomes. In aggregate, the clustering exercise confirms that the future distribution of jobs, skills and remuneration will depend less on sectoral labels than on each industry’s pace of technological adoption and its success in migrating up the competence value chain.

Absolute values—head-count, wage bills, value added—dominate the clustering output because the magnitude gaps between industries (telecoms versus food processing, for example) far exceed year-to-year fluctuations within each sector. Even ratio-based metrics such as profit-to-output or salary premia remain nearly constant inside a given industry while diverging sharply across industries, so the self-organising map continues to sort sectors mainly by size rather than by their digital-era evolution. Meaningful comparisons therefore require replacing level data with relative annual changes—percentage movements in profit, payroll, informal-labour share, and similar indicators. Converting every variable into year-on-year growth rates removes scale effects, highlights direction and momentum, and reveals which industries are accelerating, decelerating, or pivoting toward new business models under digitalisation.

Switching the analysis from absolute values to year-on-year percentage movements uncovers a markedly different landscape of sector dynamics. Once each variable is converted into an annual growth rate, the self-organising map begins to highlight momentum rather than magnitude, grouping industries by how rapidly—and in which direction—they are responding to digitalisation. The resulting clusters now reflect shared trajectories of change: some sectors advance in output and value added while simultaneously tightening workforce size, others post salary gains without accompanying productivity improvements, and a few register across-the-board slowdowns.

Figure 7’s heat maps illustrate these emergent patterns: cooler tones tracking left to right reveal sectors where employment shrinks but wages climb, whereas warmer bands in the opposite diagonal capture high-velocity expansions in both revenue and payroll. Because each hexagon represents a single industry-year observation, the visual continuity (or abrupt shifts) across adjacent cells signals whether a sector’s digital transformation is steady, volatile or stalled.

To translate the map’s colour gradients into a more formal taxonomy, observations are allocated to six discrete clusters. Table 4 summarises the allocation year by year, showing, for example, how high-tech services like telecommunications migrate from one cluster to another as they accelerate wage growth in the late 2010s, while export-oriented manufacturing branches oscillate between clusters that correspond to profit compression or modest recovery. The temporal spread across clusters confirms that digitalisation does not push industries along a single linear path; instead, each branch experiences episodic jumps or regressions depending on its investment cycle, global demand conditions and capacity for workforce reskilling.

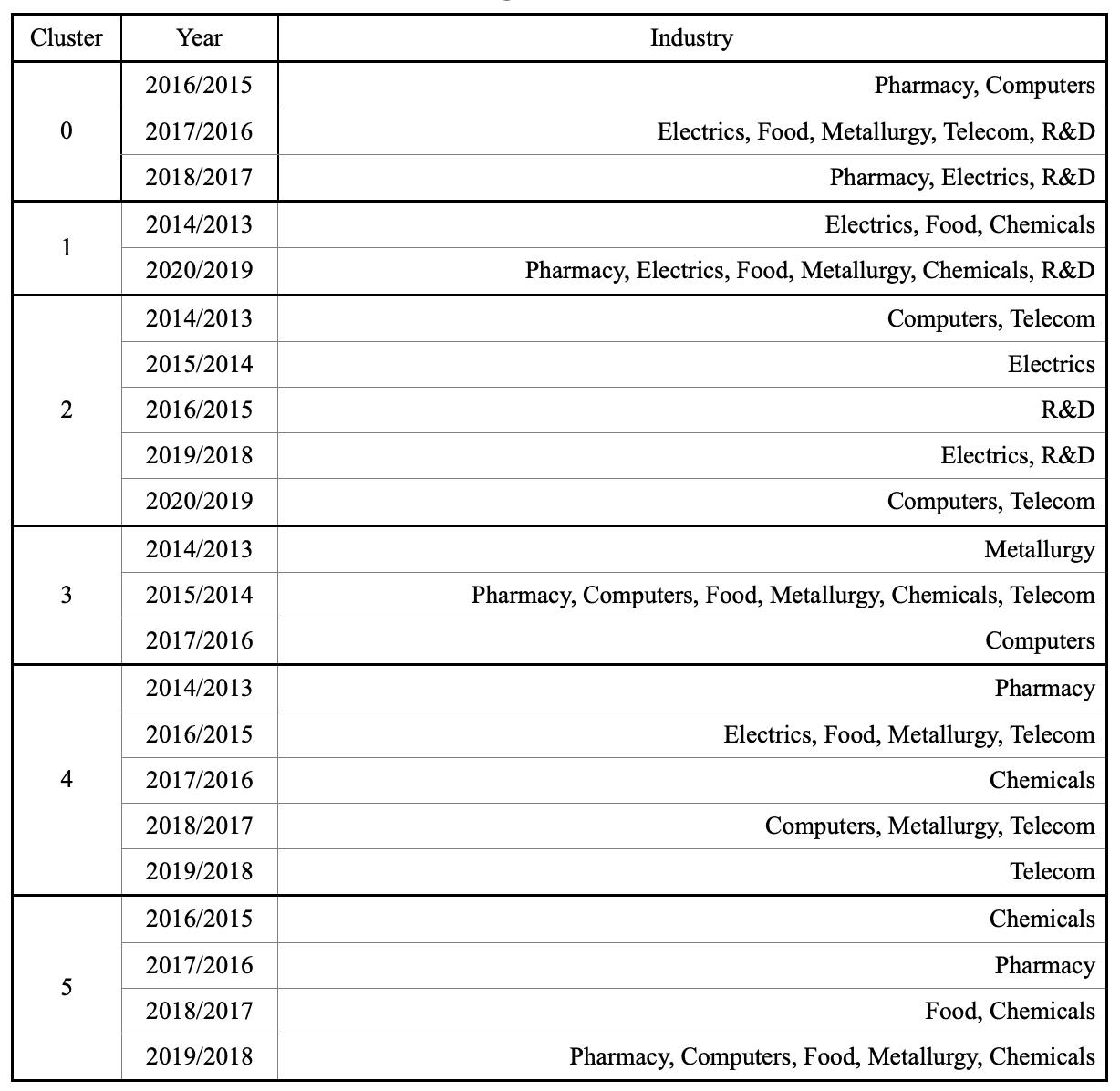

By isolating the pulse of annual change rather than static size, the revised clustering captures the real-time pulse of structural adjustment. It clarifies which industries are building momentum toward higher-value, digitally enabled operating models and which remain locked in low-growth patterns that risk reinforcing the ‘dying profession’ narrative.

Table 4 shows that cluster 1—occupying the lower-left quadrant of the Kohonen map—captures almost every industry in just two observation windows: the 2014 / 2013 and 2020 / 2019 intervals. Both moments coincide with severe external shocks: the onset of Russian military aggression in 2014 and the first year of the COVID-19 pandemic in 2020. During these crisis years, digital-intensive branches such as computer manufacturing and telecommunications shift only slightly, appearing in the adjacent cluster 2 but still anchored to neurons bordering cluster 1. Pharmaceutical production settles into the neighbouring corner of cluster 4, indicating that—across the indicator suite—every sector gravitates toward the same low-growth zone when macro-economic stress peaks.

The common signature of those two intervals is muted expansion in both nominal output and headline wages, despite sharp hryvnia devaluation that would otherwise inflate figures recorded in local currency. Employment variables reveal sharper contrasts. High-tech manufacturing and, even more, high-tech services display the steepest contractions in full-time and contract staff during the crisis years, whereas large, asset-heavy industrial exporters shed labour only marginally. Outside the shock windows, the pattern reverses: digital-centric sectors lead on head-count and contractor growth while traditional industries move sluggishly.

The disparity reflects organisational agility. High-tech service providers can reduce or add staffing rapidly, often shifting talent to remote arrangements; heavy manufacturing, in contrast, retains fixed personnel because plant operations cannot run without on-site labour. Pandemic-related lockdowns amplified this gap: factories required physical presence, limiting layoffs, while knowledge workers transitioned online, prompting a temporary employment dip before digital demand rebounded.

Consequently, cluster placement along the Kohonen map functions as a proxy for digital adaptability. Cells in the lower-left register significant structural re-tooling under duress—fewer employees, lower pay, but accelerated technology adoption—whereas those on the opposite, right-hand edge correspond to years of relative economic calm (2015–2018) when output and payroll recovered in traditional sectors and digital urgency receded. In effect, the map portrays a spectrum: crisis-driven, technology-enabled adjustment on one side; capital-intensive, inertia-bound stability on the other.

Research on the impact of employment indicators in the field of high-tech activities on indicators of macroeconomic dynamics

Recent trend-line projections for Ukraine’s economy indicate that, even after accounting for external shocks, gross domestic product (GDP) and gross value added (GVA) have followed a broadly linear, upward trajectory since 2013. Extrapolating that path through 2022 produces three plausible outlooks: an optimistic band that carries the post-2020 rebound forward at the upper confidence limit, a baseline projection that continues along the central trend, and a pessimistic band that flattens toward the lower limit.

The modelling assumes no structural breaks; it therefore treats incremental productivity gains and steady labour-force participation as the main growth engines. A closer reading suggests that the country’s ability to land in—or above—the upper confidence band hinges on how efficiently high-tech industries deploy human capital. Historical data already show that shifts in head-count, wage levels and skill composition inside the digital sector propagate into aggregate value creation with short lags. Expanding employment in research, telecommunications and advanced manufacturing—while simultaneously upgrading the competence mix—has the potential to lift total factor productivity, widen the GVA base and keep GDP growth nearer the optimistic path. Conversely, a failure to modernise workforce structure could lock macro-indicators into the baseline or even the pessimistic track. Hence, labour optimisation within the high-tech segment emerges as a practical lever for tilting national output toward the upper end of the forecast spectrum.

To test whether employment composition in digital-intensive activities can materially shift Ukraine’s macro path, multifactor regressions were estimated with gross domestic product (GDP) and gross value added (GVA) as dependent variables. Five explanatory variables capture both scale and quality of labour in high-tech production and service domains:

- Х1 – the head-count of full-time staff;

- Х2 – that head-count expressed as a share of the nation’s total full-time employment;

- Х3 – the number of contract and part-time workers hired under civil-law agreements;

- Х4 – the share of those flexible workers in total staff;

- Х5 – the nominal monthly wage, a proxy for skill depth and productivity.

Coefficients obtained for the digital segment reveal a strong elasticity of both GDP and GVA with respect to Х1 and, even more, to Х5, confirming that each incremental unit of skilled employment delivers a disproportionately large addition to national output. By contrast, similar regressions run for export-oriented heavy industries show far lower elasticities and, in some cases, statistically insignificant wage terms—evidence that productivity gains there are driven primarily by capital rather than human capital. The share variables Х2 and Х4 are significant at the ten-percent level in the high-tech model but drop out in the comparative export models, indicating that where people work inside the broader economy matters almost as much as how many are employed.

Taken together, the regression diagnostics—high adjusted R-squared values, low variance-inflation factors and Durbin–Watson statistics near two—suggest that employment optimisation in technology-rich activities can move the overall economy toward the optimistic GDP/GVA trajectory shown earlier. In practical terms, policies that enlarge the pool of full-time digital specialists, encourage legally registered flexible contracts and continue to lift median tech-sector wages are likely to push aggregate output closer to the upper confidence band, whereas failure to do so would leave growth tracking the baseline or lower bound.

Elasticity diagnostics sharpen the picture of how labour-market variables translate into headline growth. When GDP and GVA are regressed on workforce scale, mix and pay, the share of formally employed staff inside specific high-tech and export pillars emerges as the single most powerful booster of macro performance. In pharmaceutical manufacturing, metallurgy, information-and-telecommunications services and research-and-development, even a one-percentage-point rise in the sector’s proportion of total full-time employment yields a markedly larger percentage increase in both GDP and GVA than any other factor in the model. Put differently, every additional formally contracted specialist embedded in these activities carries an outsized productivity dividend for the economy as a whole.

By contrast, the balance between registered and non-registered labour exerts a more nuanced influence. Computer-hardware and optical-equipment producers show a negative elasticity on the non-registered share, implying that heavier reliance on civil-law contractors or external part-timers suppresses their contribution to national output. The chemicals industry displays the opposite pattern: a small expansion of flexible hiring correlates with a positive macro effect, probably because periodic access to specialised project talent can unlock process innovations without inflating fixed payrolls. These asymmetries suggest that workforce-formalisation campaigns should be sector-specific rather than blanket policies.

Surprisingly, average nominal pay—used here as a proxy for skills and labour quality—shows only secondary explanatory power once head-count structure is controlled for. In most cases the elasticity of GDP or GVA with respect to salaries is small and statistically fragile, indicating that qualification premiums matter less than whether employees are fully integrated into core operations versus held at arm’s length on temporary contracts.

Taken together, the elasticity matrix points to three high-leverage levers for achieving the optimistic GDP/GVA path outlined earlier:

- Expand formal, full-time head-count in digital and science-driven activities, where every incremental employee lifts value creation well beyond proportionality.

- Tighten or tailor flexible-work regulations by sector, reducing non-registered reliance in computer-hardware manufacturing while allowing targeted contractor growth in chemicals and similar project-intensive fields.

- Re-allocate labour-market incentives away from across-the-board wage subsidies toward measures that anchor skilled workers inside high-multiplying sectors—for example, tax credits tied to net additions of formally contracted STEM staff.

If policy makers succeed in shifting employment structure along these lines, the model indicates a materially higher probability of the economy tracking the upper-confidence trajectory for both GDP and GVA over the medium term.

Conclusions

A critical synthesis of contemporary research positions the digital economy as a pivotal force reshaping labour markets at every level—from single occupations to entire national industries. As digital platforms scale and breakthrough technologies diffuse, the traditional job system fragments: some roles are absorbed by automation, while new, often interdisciplinary, professions gain traction. Within this emerging landscape, employment transforms along two simultaneous dimensions. Constructive change manifests through the growth of “rising-star” occupations concentrated in high-tech manufacturing and services, where digital products are both created and consumed. Destructive change, by contrast, appears in the contraction of “dying” roles whose functions migrate to algorithms, smart machines or cloud-based workflows.

Empirical evidence drawn from International Labour Organization datasets indicates that these twin dynamics have not yet produced a net decline in work. Globally, and across Europe and Ukraine in particular, labour-force participation remains broadly stable, and unemployment continues to edge downward, delaying any predicted “jobless future.” At the same time, cluster analysis conducted on Ukrainian industry data reveals a stark divergence in performance metrics. High-tech services—especially information-and-telecommunications and research-and-development—exhibit stronger profitability and wage growth than either high-tech manufacturing or export-oriented heavy industries.

To explain these differences, the study models gross domestic product and gross value added as functions of employment scale and composition. Multifactor regressions show that the formal share of full-time staff in pharmaceuticals, ICT and R&D delivers the largest positive elasticity with respect to macroeconomic output, while average wages prove a weaker predictor once head-count and registration status are controlled for. In computer hardware, greater reliance on non-registered labour correlates with diminished macro impact, whereas a moderate expansion of flexible contracts in chemicals appears to support productivity gains. These findings suggest that labour-market policies must be sector-specific: formalisation efforts should prioritise digital manufacturing, whereas project-based industries may benefit from carefully regulated contractor pools.

Scenario forecasts for 2021–2022 place Ukraine’s GDP and GVA on an upward linear trend, framed by optimistic and pessimistic confidence bands. The modelling indicates that moving the economy toward the upper band depends less on across-the-board wage increases and more on optimising employment structure in technology-rich domains—specifically, expanding formally contracted digital specialists and aligning flexible-work regulation with sectoral needs. When these conditions are met, the constructive vector of digitalisation can outweigh its destructive counterpart, pushing aggregate output onto the optimistic growth path.

In sum, the Employment-XXI framework developed here suggests that sustained macroeconomic gains in the digital age will hinge on three levers: reallocating labour toward high-multiplying sectors, calibrating the mix of permanent and flexible employment by industry, and embedding skill-intensive roles at the core of value creation. Further research would benefit from integrated modelling that captures latent interactions among standard, non-standard and remote work formats, thereby refining the policy toolkit for human-centred growth in increasingly digital economies.

References

- Jia, Z., & Vattø, T. E. (2021). Predicting the path of labor supply responses when state dependence matters. Labour Economics, 71(C), Article 102004. https://doi.org/10.1016/j.labeco.2021.102004

- Van der Zwan, P., Hessels, J., & Rietveld, C.A. (2018). Self-employment and satisfaction with life, work, and leisure. Journal of Economic Psychology, 64, 73-88. https://doi.org/10.1016/j.joep.2017.12.001

- Cowling, M., Millán, J. M., & Yue, W. (2019). Two decades of European self-employment: Is the answer to who becomes self-employed different over time and countries? Journal of Business Venturing Insights, 12(C), Article e00138. https://doi.org/10.1016/j.jbvi.2019.e00138

- Nolan, A., & Barrett, A. (2019). The role of self-employment in Ireland’s older workforce. The Journal of the Economics of Ageing, 14(C), Article 100201. https://doi.org/10.1016/j.jeoa.2019.100201

- Patel, Pankaj C. & Wolfe, Marcus T. (2019). Money might not make you happy, but can happiness make you money? The value of leveraging subjective well-being to enhance financial well-being in self-employment. Journal of Business Venturing Insights, 12(C), Article e00134. https://doi.org/10.1016/j.jbvi.2019.e00134

- Stenard, B. S. (2019). Are transitions to self-employment beneficial? Journal of Business Venturing Insights, 12(C), Article e00131. https://doi.org/10.1016/j.jbvi.2019.e00131

- Lee, N., & Clarke, S. (2019). Do low-skilled workers gain from high-tech employment growth? High-technology multipliers, employment and wages in Britain. Research Policy, 48(9), Article 103803. https://doi.org/10.1016/j.respol.2019.05.012

- Sheehan, P., & Shi, H. (2019). Employment and Productivity Benefits of Enhanced Educational Outcomes: A Preliminary Modelling Approach. Journal of Adolescent Health, 65(1), 44-51. https://doi.org/10.1016/j.jadohealth.2019.03.025

- He, Y., Peng, X., & Xu, H. (2020). Overeducation, market recognition, and effective labour supply. China Economic Review, 59(C), Article 101384. https://doi.org/10.1016/j.chieco.2019.101384

- Kergroach, S. (2017). Industry 4.0: New Challenges and Opportunities for the Labour Market. Foresight and STI Governance, 11(4), 6–8. https://doi.org/10.17323/2500-2597.2017.4.6.8

- Wadley, D. (2021). Technology, Capital Substitution and Labor Dynamics: Global Workforce Disruption in the 21st Century? Futures, 132, Article 102802. https://doi.org/10.1016/j.futures.2021.102802

- Zhang, F., Meng, L., Sun, W., & Si, Y. (2021). Information technology and the labor market in China. Economic Analysis and Policy, 72(C), 156-168. https://doi.org/10.1016/j.eap.2021.06.015

- Giddens, A. (2002). Runaway World: How Globalization is Reshaping Our Lives. Profile Books.

- Rifkin, J. (1995). The end of work: The decline of the global labor force and the dawn of the post-market era. G. P. Putnam’s Son. http://pinguet.free.fr/rifkin1995.pdf

- Hines, A. (2019). Getting Ready for a Post-Work Future. Foresight and STI Governance, 13(1), 19–30. https://doi.org/10.17323/2500-2597.2019.1.19.30

- Kolot, A., & Herasymenko, O. (2017). Market, state and business in coordinates of the new economy. Problems and Perspectives in Management, 15(3), 76-97. http://dx.doi.org/10.21511/ppm.15(3).2017.07

- 17.Kolot, A., Kozmenko, S., Herasymenko, O., & Štreimikienė, D. (2020). Development of a Decent Work Institute as a Social Quality Imperative: Lessons for Ukraine. Economics and Sociology, 13(2), 70-85. https://doi.org/10.14254/2071-789X.2020/13-2/5

- Kolot, A., Herasymenko, O., & Yarmolyuk-Kröck, К. (2020). Impact of COVID-19 pandemic on economic development and labor in Ukraine. Friedrich Ebert Stiftung. http://library.fes.de/pdf-files/bueros/kiew/17372.pdf

- 19.Poruchnyk, A., Kolot, A., Mielcarek, P., Stoliarchuk, Y., & Ilnytskyy, D. (2021). Global economic crisis of 2020 and a new paradigm of countercyclical management. Problems and Perspectives in Management, 19(1), 397–415. https://doi.org/10.21511/ppm.19(1).2021.34

- OECD. (2015). Data-Driven Innovation: Big Data for Growth and Well-Being. OECD Publishing. http://dx.doi.org/10.1787/9789264229358-en

- Kenney, M., & Zysman, J. (2016). The Rise of the Platform Economy. Issues in Science and Technology, 32(3), 61-69. https://issues.org/rise-platform-economy-big-data-work/

- Fernández-Macías, E., Hurley, J., & Bisello, M. (2016). What do Europeans do at work? A task-based analysis: European Jobs Monitor. European Foundation for the Improvement of Living and Working Conditions. https://www.eurofound.europa.eu/publications/report/2016/what-do-europeans-do-at-work-a-task-based-analysis-european-jobs-monitor-2016

- Frey, C. B., & Osborne, M. A. (2017). The future of employment: How susceptible are jobs to computerisation? Technological Forecasting and Social Change, 114, 254–280. https://doi.org/10.1016/j.techfore.2016.08.019

- Huateng, M., Zhaoli, M., Deli, Y., & Hualei, W. (2021). The Chinese Digital Economy (G. Kaitian, & S. Xiao, Eds.). Palgrave Macmillan. https://doi.org/10.1007/978-981-33-6005-1

- Sorgner, A. (2017). The Automation of Jobs: A Threat for Employment or a Source of New Entrepreneurial Opportunities? Foresight and STI Governance, 11(3), 37–48. https://doi.org/10.17323/2500-2597.2017.3.37.48

- 26.Seidl da Fonseca, R. (2017). The Future of Employment: Evaluating the Impact of STI Foresight Exercises. Foresight and STI Governance, 11(4), 9–22. https://doi.org/10.17323/1995-459X.2016.4.9.22

- 27.Manyika, J., Chui, M, Miremadi, M., Bughin, J., George, K., Willmott, P., & Dewhurst, M. (2017, January 12). Harnessing automation for a future that works. McKinsey Global Institute. https://www.mckinsey.com/featured-insights/digital-disruption/harnessing-automation-for-a-future-that-works

- 28.Fossen, F., & Sorgner, A. (2019). Mapping the Future of Occupations: Transformative and Destructive Effects of New Digital Technologies on Jobs. Foresight and STI Governance, 13(2), 10–18. https://doi.org/10.17323/2500-2597.2019.2.10.18

- 29.Chang, J.-H., Rynhart, G., & Huynh, P. (2016). ASEAN in Transformation: The Future of Jobs at Risk of Automation. Bureau for Employers’ Activities. International Labour Organization. https://www.ilo.org/actemp/publications/WCMS_579554/lang--en/index.htm

- Reese, B. (2019, January 1). AI will create millions more jobs than it will destroy. Here’s how. Singularity Hub. https://singularityhub.com/2019/01/01/ai-will-create-millions-more-jobs-than-it-will-destroy-heres-how/

- 31.Azmuk, N.A. (2019). Transformatsiia zainiatosti pry perekhodi do tsyfrovoi ekonomiky: hlobalni vyklyky ta stratehii adaptatsii [Transforming employment at the transition to the digital economy: global challenges and adaptation strategies]. Znannia. https://iie.org.ua/monografiyi/transformacija-zajnjatosti-pri-perehodi-do-cifrovoi-ekonomiki-globalni-vikliki-ta-strategii-adaptacii/ [in Ukrainian].

- Morrison, M. (2022, January 19). History of SMART Objectives. RapidBI. https://rapidbi.com/history-of-smart-objectives/

- 33.Novikova, O. F., Zaloznova, Yu. S., Amosha, O. I., Khandii, O. O., Azmuk, N. A., Ostafiichuk, Ya. V., Shamileva, L. L., Pankova O. V., Novak, I. M., Shastun, A. D., Kasperovych, O. Yu., Ishchenko, O. V., Krasulina, Ya. Ie., Amelicheva, L. P., & Kompaniiets, V. V. (2022). Transformatsiia sotsialno-trudovoi sfery v umovakh tsyfrovizatsii ekonomiky [Transformation of the social and labor sphere in the conditions of digitalization of the economy]. NAN Ukrainy, In-t ekonomiky prom-sti. https://iie.org.ua/monografiyi/transformacija-socialno-trudovoi-sferi-v-umovah-cifrovizacii-ekonomiki/ [in Ukrainian]

- Kolot, A. M., & Herasymenko, O. O. (2021). Pratsia XXI: filosofiia zmin, vyklyky, vektory rozvytku [Work XXI: philosophy of change, challenges, vectors of development]. KNEU. https://ir.kneu.edu.ua/handle/2010/36870?show=full [in Ukrainian]

- 35.International Labour Organization. (2019). Work for a brighter future – Global Commission on the Future of Work. https://www.ilo.org/wcmsp5/groups/public/---dgreports/---cabinet/documents/publication/wcms_662410.pdf

- 36.Frey, C.B., Osborne, M. (2015). Technology at work: The future of innovation and employment. Citi Global Perspectives and Solutions. https://www.oxfordmartin.ox.ac.uk/downloads/reports/Citi_GPS_Technology_Work.pdf

- Manyika, J., Chui, M, Miremadi, M., Bughin, J., George, K., Willmott, P., & Dewhurst, M. (2017, January 12). A future that works: Automation, employment, and productivity. McKinsey Global Institute. https://www.mckinsey.com/featured-insights/digital-disruption/harnessing-automation-for-a-future-that-works/de-DE

- 38.Organization for Economic Co-operation and Development. (2016). Policy Brief on the Future of Work – Automation and independent work in a digital economy. OECD Publishing. https://www.oecd.org/els/emp/Policy%20brief%20-%20Automation%20and%20Independent%20Work%20in%20a%20Digital%20Economy.pdf

- 39.World Bank. (2016). World Development Report 2016: Digital dividends. https://doi.org/10.1596/978-1-4648-0671-1

- 40.World Economic Forum. (2018). The Future of Jobs Report. https://www3.weforum.org/docs/WEF_Future_of_Jobs_2018.pdf

- United Nations, Department of Economic and Social Affairs, Population Division. (2017). World Population Prospects: The 2017 revision, key findings and advance tables (Working Paper No. ESA/P/WP/248). https://desapublications.un.org/publications/world-population-prospects-2017-revision

- International Labour Organization. (1991-2021). World Employment and Social Outlook Data Finder [Data set]. Retrieved July 10, 2022, from https://www.ilo.org/wesodata

- Kolot, A. M., & Herasymenko, O. O. (2019). Social and labor development in the XXI century: to the nature of global changes, new opportunities, limitations and challenges. Demography and social economy, 1(35), 97–125. [in Ukrainian]

- Kohonen, T. (2001). Self-Organizing Maps (3rd ed.). Springer.

- Kobets, V., & Novak, O. (2021). EU countries clustering for the state of food security using machine learning techniques. Neuro-Fuzzy Modeling Techniques in Economics, 10, 86-118. http://doi.org/10.33111/nfmte.2021.086

- State Statistics Service of Ukraine. (2013-2020). Statystychnyi zbirnyk «Pratsia Ukrainy» [Statistical collection “Labor of Ukraine”] [Data set]. Retrieved January 7, 2022, from https://www.ukrstat.gov.ua/druk/publicat/Arhiv_u/11/Arch_pu_zb.htm

- State Statistics Service of Ukraine. (2013-2020). Statystychnyi zbirnyk «Natsionalni rakhunky Ukrainy» [Statistical collection “National accounts of Ukraine”] [Data set]. Retrieved January 7, 2022, from https://www.ukrstat.gov.ua/druk/publicat/Arhiv_u/03/Arch_nr.htm

- State Statistics Service of Ukraine. (2013-2020). Tablytsia «vytraty-vypusk» Ukrainy u tsinakh spozhyvachiv [Ukraine’s consumption-output table at consumer prices] [Data set]. Retrieved January 7, 2022, from https://www.ukrstat.gov.ua/operativ/operativ2006/vvp/vitr_vip/vitr_u/arh_vitr_u.html

Tell us about your project needs

.png)

.png)